How To Perform Fundamental Analysis Of Stocks

- 5m•

- 2,300•

- Updated 14 Aug 2023

Fundamental analysis, we try to assess a company’s future prospects based on a scrutiny of its financial statements. We try to project its future earnings and based on them, estimate its value. We will take up these concepts individually in this section.

However, we will first explain a concept called efficient market hypothesis, which seeks to explain why investors line up to buy stocks of companies that are expected to perform well and push their values up.

What Is Efficient Market Hypothesis?

Equity investors, like you, like to invest in companies that they believe will achieve high earnings growth in the future. This is because high growth companies come with a higher future dividend paying potential. This, in turn, invites more investors to buy them. It ultimately leads to an appreciation of the stock price.

Assumptions Of Efficient Market Hypothesis

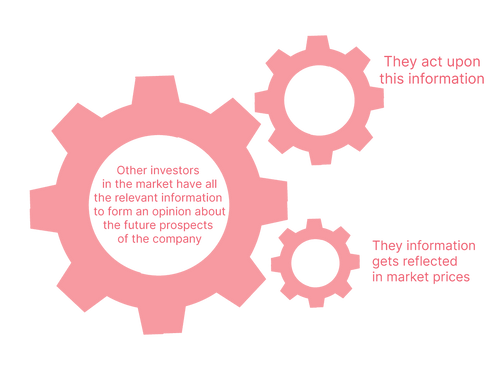

This philosophy is based on three assumptions: other investors in the market have all the relevant information to form an opinion about the future prospects of the company; they act upon this information, and this information gets reflected in market prices.

A market that displays these characteristics is called an efficient market. In such markets, all investors are privy to all the information pertaining to a company. They all use the same set of information to make their investment decisions. As a result, nobody can make more profit than the other and all the relevant information is reflects in market prices. This was the central idea of Eugene Fama’s efficient market hypothesis of the 1960s.

Fundamental analysts use three categories of data—historical data, publically known information about the market (such as announcements made by the management in the media and the annual reports released by it) and private information (or the information known only to a select few, owing to their position with the organization).

According to Fama, in an efficient market, there is no private information. All the information is available for free and known to all. As a result, all investors act on this common set of information and make equal profits. No one is able to ’beat the market’ or earn ‘abnormal profits’ based on special information or analysis. Also, there is no time lag between the release of the information and its influence on prices.

Fama’s theory has earned widespread disrepute because what it proposed appears to be a fantasy. No two investors achieve the same returns in a market. Every year, a horde of investors earn greater returns than benchmark indices, such as the BSE Sensex. Further, not all information is available to everybody. There are people, such as top employees of the company that are privy to classified information, not known to all. They sometimes use it unethically to make greater profits than other people. This practice is called insider trading. It is punishable by law. Further, institutions like investment banks and stock brokerages, deduce vital information from the analysis of companies. This is only available to their clients for a price. Thus, information is not free either. It is clear that Fama’s treatise regarding markets being efficient is therefore questionable. Even so, his theory is appreciated because it paints a picture of what could happen if market conditions were perfect. Just that probably, current market conditions aren’t perfect.

Introduction To Stock Valuation

Now that we have established that the market conditions we operate under are not perfect, it is clear that equity analysis can generate superior returns for you compared to the market. Let’s then proceed towards the process of analyzing companies. This portion deals with the approaches to calculating the tfair or intrinsic value of a stock.

Fair or intrinsic value of a stock is the price the stock should actually be trading at according to your analysis. You can compare it with its current market price to ascertain whether it is overvalued, undervalued or fairly valued. You would like to buy a stock that is undervalued, because its price should appreciate to your estimate of fair value, earning you a profit in the process. If you own a stock that you think is overvalued, you sell it. As for fairly valued stocks, you’d best leave them alone.

There are three techniques used for the valuation of equity shares:

-

Present Value Models:

Present value models are based on the principal that since shareholders are joint-owners of the company, its future earnings belong to them. The combined value of these earnings, in terms of today’s money, should therefore be the value of these equity shares.

The value of money changes with time. Rs 100 will not be worth the same in ten years’ time as it is today. Similarly, the value of future income projected for a future period will be different today.

To account for this, future incomes are divided by a specific discount rate to calculate their value as of today. This is known as time value of money. The present value model has different variants. Each of them uses a different concept of future income for discounting. These include dividend, residual income and free cash flows. The model that uses dividends is the most straight forward and commonly used. We will explain this in a later section.

-

Relative Value (Multiplier) Models:

A company can also be valued relative to the value of other, similar companies. In this case, the market price of its rivals is compared with one of their fundamentals, such as sales, book value of equity and net income. The ratio is then applied to the concerned company to estimate its value. The ratios used for this purpose are called price multiples.

-

Asset-Based Valuation:

In this model, the value of a company is based on the market value of its assets and liabilities. The market value of liabilities (not including equity) is subtracted from the market value of assets to arrive at the value of equity. For the model to work, most of the assets of the company should be tangible long-term assets. This model is rarely used.

Introduction To Financial Statement Analysis

The financial performance of a company is organized and reported in the form of financial statements. There are three important statements presented in the annual and quarterly reports of a company: the income statement, the balance sheet and the cash flow statement. A brief description of each of these is present below.

-

The Income Statement:

The income statement deals with the incomes and expenses of a company during a given financial year. It classifies them into various parts based on their nature. Expenses are subtracted from incomes to arrive at the profit for the year.

When analyzing the income statement, you should be concerned about the stability and future growth potential of incomes and expenses. Companies are evaluated on the basis of income from their ‘core businesses’. Although companies also earn revenue from other sources from time to time, these sources are not considered stable and truly representative of the efficiency of the company’s operations.

Expenses-wise, you are again interested in looking at the categories of expenses, their criticality to the business, prospects of their recurrence and their role in increasing future earnings.

-

The Cash Flow Statement:

This statement specifically talks about the cash position of a company. It divides the company’ activities into three categories—operating, investing and financing, and gives an account of the cash flowing in and out of the business on account of these.

The importance of the cash flow statement dwells on the fact that while a company earns and spends a lot of funds, as accounted for in the income statement, a lot of these flow are non-cash. A lot of these flows inspire the hope of receiving or paying cash in future, whereas others don’t entail a flow at all. The statement removes this confusion by specifically stating the sources and uses of cash in the current period. Ideally, companies would be best placed if they generate enough cash from operations to finance their investing activities. Bringing in cash from financing activities to fund the other two implies an increase in the level of liabilities.

-

The Balance Sheet:

This is the other most critical financial statement. It talks about the assets and liabilities of the business. Unlike the income statement, the balance sheet reflects the state of the assets and liabilities of a business at a particular point in time and not over a period of time.

A company needs certain assets to run its business smoothly. These are financed by certain liabilities—debt and equity. For a company to be profitable, the revenue generated from these assets should be greater than the amount required to repay the liabilities incurred to acquire them.

This is what you should try and ascertain from the balance sheet. You are concerned about the nature of the assets and their future revenue generation potential. At the same time, you are also concerned about the sustainability of debt. Too much debt will pressurize the company to earn beyond its potential to repay this debt. This is a dangerous and unsustainable proposition.